This article is provided for general informational and educational purposes only and does not constitute legal advice. Laws, insurance requirements, and fault-determination rules vary by jurisdiction and individual circumstances. Readers should consult a licensed attorney or other qualified professional for guidance specific to their situation.

Introduction

After a car accident, one of the most important questions in the insurance claims process is how fault is determined. Fault plays a central role in whether a claim is paid, how compensation is allocated, and which insurance policies apply.

Many people assume fault is decided quickly or based on a single factor, such as a police report or an initial statement. In practice, insurance companies evaluate fault through a multi-step review process that relies on documentation, timelines, and consistency across records rather than on any one piece of information alone.

This article explains how insurance companies commonly assess fault after a car accident, what sources they typically review, and why fault determinations may evolve as a claim progresses. The goal is to provide general educational context about insurance review practices, not to assess fault in any specific case.

Car Accident Claims 101 — Your Complete Guide to the Claims Process

Why Fault Matters in Car Accident Claims

Fault determines how responsibility for damages is allocated after a collision. Depending on the jurisdiction and insurance system involved, fault may affect:

-

Which insurance policy applies

-

Whether a claim is paid at all

-

How compensation is calculated

-

Whether recovery is reduced due to shared responsibility

Because fault can influence multiple aspects of a claim, insurers generally evaluate it carefully and may revisit the issue as additional information becomes available.

The Insurance Company’s Role in Fault Evaluation

Insurance companies assess fault as part of their obligation to review claims under the terms of the applicable policy. This evaluation is conducted by claims adjusters and may involve internal review guidelines, documentation standards, and supervisory oversight.

Fault determination is typically evidence-based, meaning insurers rely on written records and objective materials rather than informal explanations or assumptions.

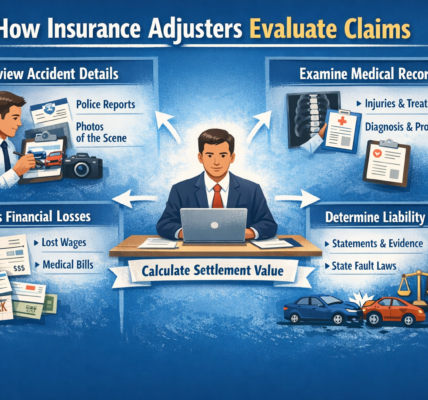

Sources Commonly Reviewed When Determining Fault

Accident and Police Reports

One of the first documents reviewed is often an accident or police report prepared at the scene. These reports may include:

-

Date, time, and location of the collision

-

Identification of drivers and vehicles involved

-

Statements from drivers and witnesses

-

Observations regarding road, traffic, and weather conditions

-

Notes regarding citations or observed violations

While police reports are influential, they do not always determine fault on their own. Insurers typically treat them as one component of a broader review.

Statements and Claim Documentation

Insurance companies often review statements provided during the claims process, including:

-

Initial claim reports

-

Recorded or written statements

-

Follow-up correspondence

These statements are usually evaluated for consistency over time and compared against other documentation rather than considered in isolation.

Photographs and Video Evidence

Visual evidence can play a significant role in fault assessment. Insurers may review:

-

Photographs of vehicle damage

-

Images of the accident scene

-

Dashcam or traffic camera footage

-

Surveillance or third-party video, when available

Damage patterns and vehicle positioning can help insurers understand how a collision occurred.

Vehicle Damage Assessments

Repair estimates, inspection reports, and damage photographs are often examined to assess:

-

Point of impact

-

Direction of force

-

Severity of collision

Vehicle damage documentation is commonly reviewed alongside accident reports and statements to evaluate overall consistency.

Witness Information

When available, witness statements may be reviewed as independent observations. Insurers typically consider:

-

Whether witnesses are neutral or involved parties

-

Whether accounts align with physical evidence

-

The level of detail and consistency provided

Witness information is usually weighed together with other evidence rather than treated as conclusive on its own.

How Insurance Adjusters Evaluate Claims

How Liability Is Evaluated

At-Fault Insurance Systems

In many states, car accidents are handled under an at-fault (tort) system, where the driver responsible for causing the accident is financially responsible for damages. In these systems, insurers focus heavily on determining which party was responsible for the collision.

No-Fault Insurance Systems

Some states operate under no-fault insurance systems, where certain benefits are paid by each driver’s own insurer regardless of fault, typically through personal injury protection (PIP) coverage.

Even in no-fault systems, fault may still be evaluated for:

-

Property damage claims

-

Claims exceeding no-fault thresholds

-

Situations involving serious injuries

Comparative and Contributory Negligence

Many jurisdictions recognize shared responsibility through comparative or contributory negligence rules.

-

Comparative negligence allows fault to be divided between parties

-

Contributory negligence (used in a small number of states) may limit recovery if a party is found partially responsible

Insurers apply these rules based on jurisdictional standards and the evidence available in the claim file.

Why Fault Determinations May Change Over Time

Fault evaluations are not always final at the beginning of a claim. Insurers may revise assessments as:

-

Additional documentation is submitted

-

Medical or repair records become available

-

Witness statements are clarified

-

Video or third-party evidence is obtained

Because claims develop over time, fault determinations may evolve as the record becomes more complete.

Common Reasons Fault Is Disputed

Fault disputes often arise due to:

-

Conflicting accounts of how the accident occurred

-

Lack of independent witnesses

-

Incomplete or unclear accident reports

-

Multiple vehicles or chain-reaction collisions

-

Road or weather conditions affecting interpretation

In disputed cases, insurers typically rely on documentation and consistency rather than immediate conclusions.

Multi-Vehicle and Complex Accidents

Accidents involving multiple vehicles, commercial drivers, or unusual circumstances often involve more extensive fault review. These claims may require:

-

Review of multiple insurance policies

-

Analysis of sequential impacts

-

Consideration of commercial or employer liability

As complexity increases, fault evaluation often becomes more detailed and time-consuming.

How Fault Fits Into the Overall Claim Review

Fault determination is only one part of the broader claims process. Insurers typically evaluate fault alongside:

-

Medical documentation

-

Vehicle damage assessments

-

Policy coverage terms

-

Wage or employment records, when applicable

Claims are generally reviewed as a whole rather than based on a single factor.

When Individuals Seek Additional Guidance

In some situations, individuals seek professional guidance to better understand fault determinations, documentation requirements, or insurance communications. This often occurs when:

-

Fault is disputed

-

Multiple parties are involved

-

Injuries are significant

-

Claim review becomes prolonged

The decision to seek guidance varies by circumstance and is influenced by claim complexity rather than any single issue.

Understanding No-Fault vs At-Fault Car Accident Claims

Summary

Insurance companies determine fault after a car accident using structured review processes that rely on documentation, evidence, and jurisdiction-specific rules. Commonly reviewed materials include accident reports, statements, vehicle damage records, photographs, witness information, and applicable traffic laws.

Fault determinations may change over time as additional information becomes available, and insurers generally assess fault as part of a broader claim evaluation rather than as an isolated decision.

Understanding how insurers commonly approach fault determination can help explain why certain documents are requested, why reviews take time, and why outcomes may differ between cases.

When to Hire a Lawyer After a Car Accident

Last reviewed for informational accuracy: February 2026